正在加载图片...

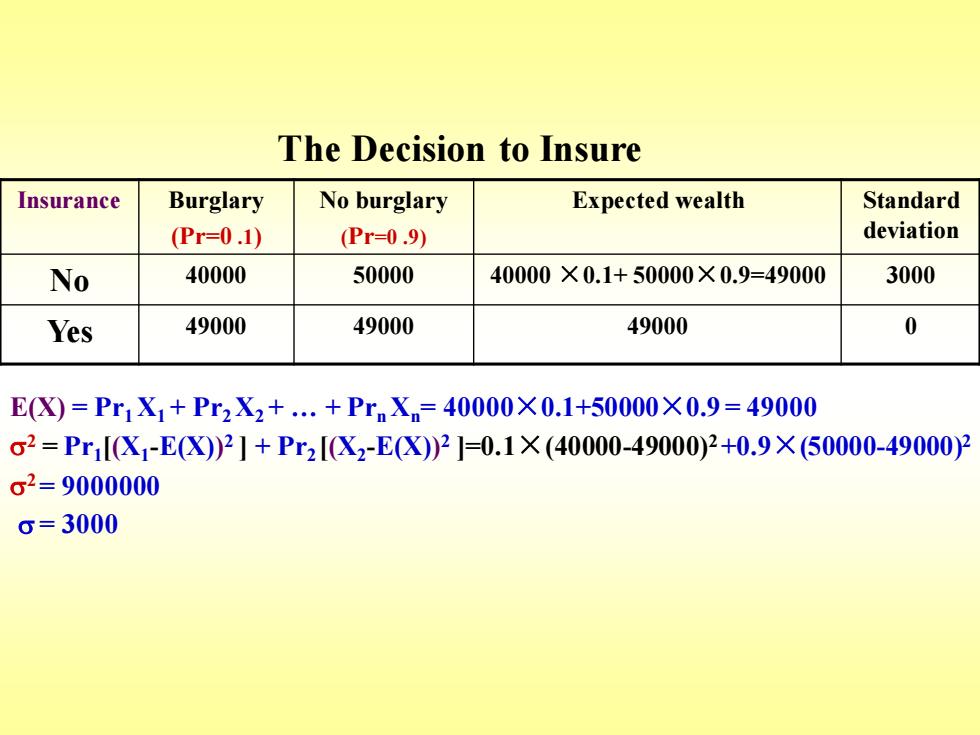

The Decision to Insure Insurance Burglary No burglary Expected wealth Standard (Pr=0.1) (Pr=0.9) deviation No 40000 50000 40000×0.1+50000×0.9=49000 3000 Yes 49000 49000 49000 0 E(X)=Pr1X1+Pr2X2+.+Pr.X.=40000×0.1+50000×0.9=49000 σ2=Pr1I(X1-EX)2]+Pr2IX2-EX)2]=0.1×(40000-49000)2+0.9×(50000-49000)2 σ2=9000000 g=3000 The Decision to Insure E(X) = Pr1 X1 + Pr2 X2 + . + Prn Xn = 40000×0.1+50000×0.9 = 49000 2 = Pr1 [(X1 -E(X)) 2 ] + Pr2 [(X2 -E(X)) 2 ]=0.1×(40000-49000) 2+0.9×(50000-49000) 2 2= 9000000 = 3000 Insurance Burglary (Pr=0 .1) No burglary (Pr=0 .9) Expected wealth Standard deviation No 40000 50000 40000 ×0.1+ 50000×0.9=49000 3000 Yes 49000 49000 49000 0