正在加载图片...

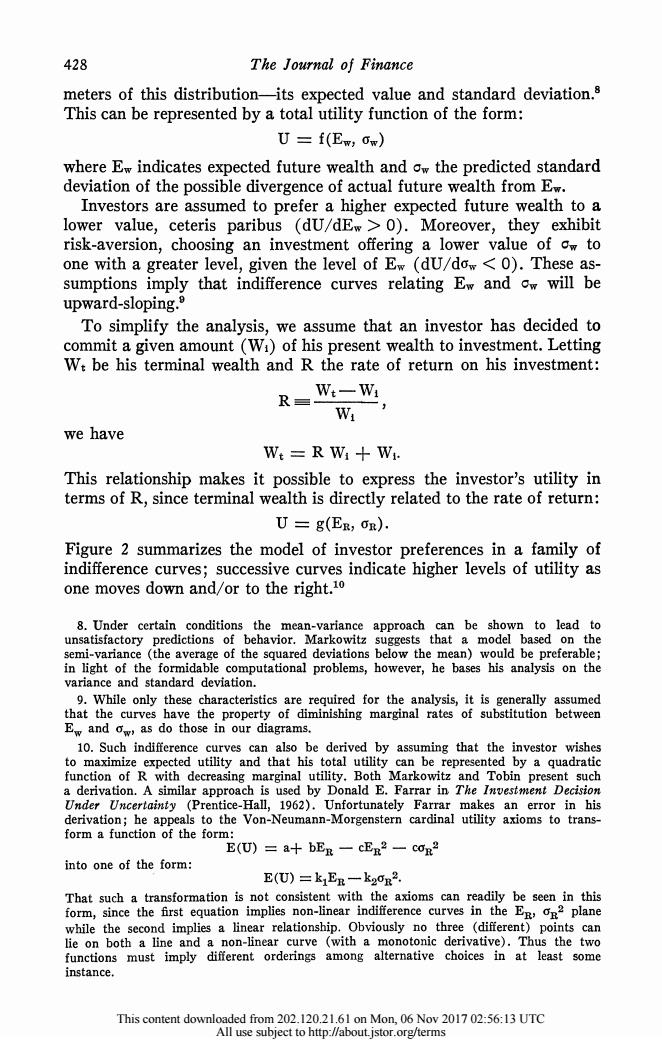

428 The Journal of Finance meters of this distribution-its expected value and standard deviation.s This can be represented by a total utility function of the form: U=f(Ew;w) where Ew indicates expected future wealth and ow the predicted standard deviation of the possible divergence of actual future wealth from Ew. Investors are assumed to prefer a higher expected future wealth to a lower value,ceteris paribus (dU/dEw>0).Moreover,they exhibit risk-aversion,choosing an investment offering a lower value of ow to one with a greater level,given the level of Ew (dU/dow<0).These as- sumptions imply that indifference curves relating Ew and cw will be upward-sloping. To simplify the analysis,we assume that an investor has decided to commit a given amount (Wi)of his present wealth to investment.Letting We be his terminal wealth and R the rate of return on his investment: R=W:一W Wi we have Wt=R Wi+Wi. This relationship makes it possible to express the investor's utility in terms of R,since terminal wealth is directly related to the rate of return: U=g(EE,OR). Figure 2 summarizes the model of investor preferences in a family of indifference curves;successive curves indicate higher levels of utility as one moves down and/or to the right.10 8.Under certain conditions the mean-variance approach can be shown to lead to unsatisfactory predictions of behavior.Markowitz suggests that a model based on the semi-variance (the average of the squared deviations below the mean)would be preferable; in light of the formidable computational problems,however,he bases his analysis on the variance and standard deviation. 9.While only these characteristics are required for the analysis,it is generally assumed that the curves have the property of diminishing marginal rates of substitution between Ew and ow as do those in our diagrams. 10.Such indifference curves can also be derived by assuming that the investor wishes to maximize expected utility and that his total utility can be represented by a quadratic function of R with decreasing marginal utility.Both Markowitz and Tobin present such a derivation.A similar approach is used by Donald E.Farrar in The Investment Decision Under Uncertainty (Prentice-Hall,1962).Unfortunately Farrar makes an error in his derivation;he appeals to the Von-Neumann-Morgenstern cardinal utility axioms to trans- form a function of the form: E(U)=a+bEg一cEa2一coh2 into one of the form: E(U)=k1Er一k20r2. That such a transformation is not consistent with the axioms can readily be seen in this form,since the first equation implies non-linear indifference curves in the Eg,oB2 plane while the second implies a linear relationship.Obviously no three (different)points can lie on both a line and a non-linear curve (with a monotonic derivative).Thus the two functions must imply different orderings among alternative choices in at least some instance This content downloaded from 202.120.21.61 on Mon,06 Nov 2017 02:56:13 UTC All use subject to http://about.jstor.org/terms428 The Journal of Finance meters of this distribution-its expected value and standard deviation.8 This can be represented by a total utility function of the form: U = f(E,, a,) where Ew indicates expected future wealth and cw the predicted standard deviation of the possible divergence of actual future wealth from Ew. Investors are assumed to prefer a higher expected future wealth to a lower value, ceteris paribus (dU/dEw > 0). Moreover, they exhibit risk-aversion, choosing an investment offering a lower value of aw to one with a greater level, given the level of Ew (dU/dow < 0). These as- sumptions imply that indifference curves relating Ew and co will be upward-sloping.9 To simplify the analysis, we assume that an investor has decided to commit a given amount (WI) of his present wealth to investment. Letting Wt be his terminal wealth and R the rate of return on his investment: R Wt Wi WI we have Wt R WI + Wi. This relationship makes it possible to express the investor's utility in terms of R, since terminal wealth is directly related to the rate of return: U = g(ER, OR) . Figure 2 summarizes the model of investor preferences in a family of indifference curves; successive curves indicate higher levels of utility as one moves down and/or to the right.10 8. Under certain conditions the mean-variance approach can be shown to lead to unsatisfactory predictions of behavior. Markowitz suggests that a model based on the semi-variance (the average of the squared deviations below the mean) would be preferable; in light of the formidable computational problems, however, he bases his analysis on the variance and standard deviation. 9. While only these characteristics are required for the analysis, it is generally assumed that the curves have the property of diminishing marginal rates of substitution between EW and aw, as do those in our diagrams. 10. Such indifference curves can also be derived by assuming that the investor wishes to maximize expected utility and that his total utility can be represented by a quadratic function of R with decreasing marginal utility. Both Markowitz and Tobin present such a derivation. A similar approach is used by Donald E. Farrar in The Investment Decision Under Uncertainty (Prentice-Hall, 1962). Unfortunately Farrar makes an error in his derivation; he appeals to the Von-Neumann-Morgenstern cardinal utility axioms to trans- form a function of the form: E(U) = a+ bER - cER2 -CR2 into one of the form: E (U) = k1 E -k2aR2. That such a transformation is not consistent with the axioms can readily be seen in this form, since the first equation implies non-linear indifference curves in the ER' aR2 plane while the second implies a linear relationship. Obviously no three (different) points can lie on both a line and a non-linear curve (with a monotonic derivative). Thus the two functions must imply different orderings among alternative choices in at least some instance. This content downloaded from 202.120.21.61 on Mon, 06 Nov 2017 02:56:13 UTC All use subject to http://about.jstor.org/terms