正在加载图片...

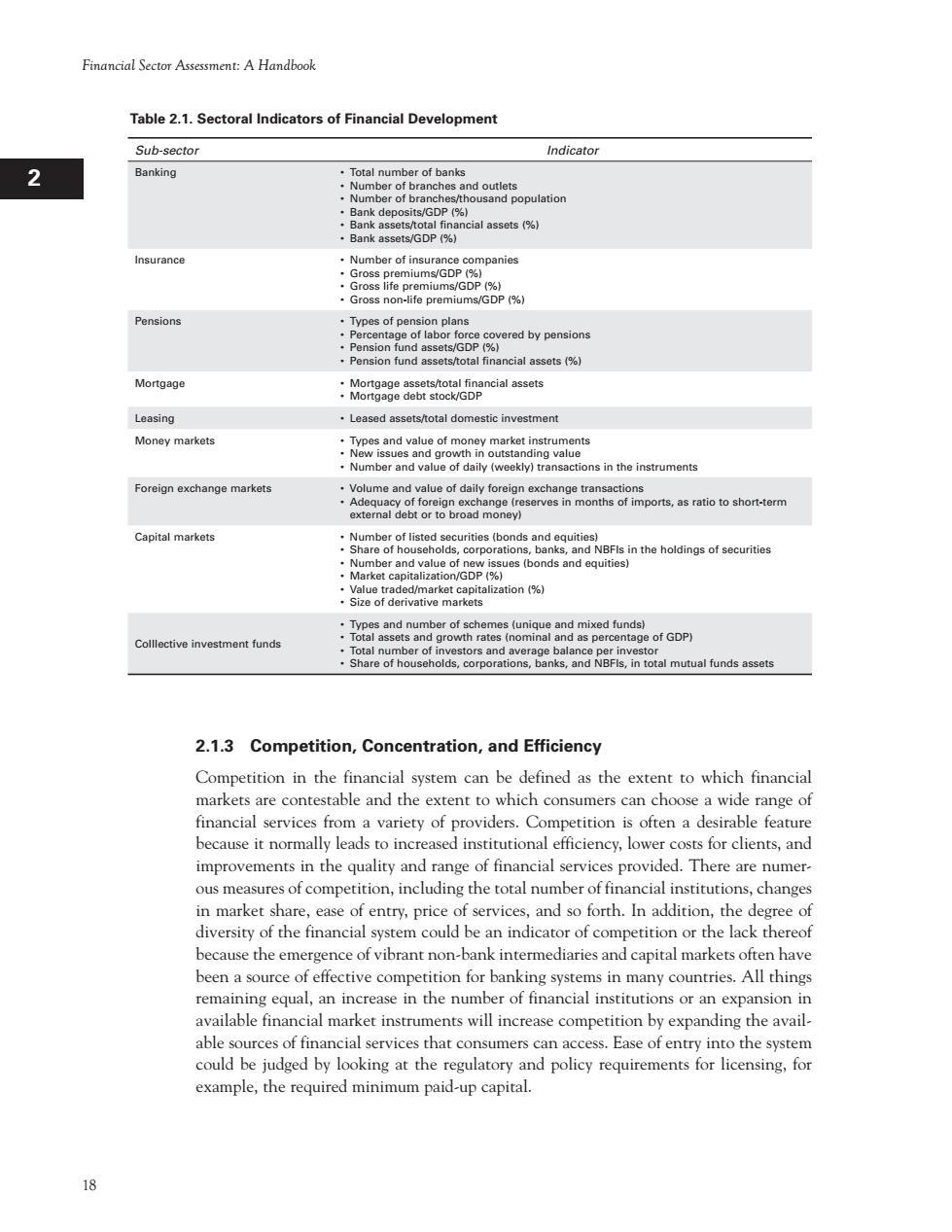

Financial Sector Assessment A handhook Table 2.1.Sectoral Indicators of Financial Development Sub-sector Indicator 2 Banking Total number of bank SDP(% Pensions M8nggeaiteueke9 asset Leasing Leased assets/total domestic investment Money markets in the instruments Foreign exchange Capital markets and value of entag of GDP) .Share of households corporations bank and in total mutual funds assets 2.1.3 Competition,Concentration,and Efficiency Competition in the financial system can be defined as the extent to which financial markets are contestable and the nt to which consumers can choose a widera financial often a desi ange of es fror able featur because it normally efficiency,lower for clients,and improvements in the quality and range of financial services provided.There are numer. ous measures of competition,including the total number of financial institutions,changes in market share,ease of entry,price of services,and so forth.In addition,the degree of diversity of the financial system could be an indicator of competition or the lack thereof because the emergence of vibrant non-bank intermediaries and capital markets often have been a source of effective competition for bankins g systems in many countries.All thing remaining increase in the number of f cial institution sio a vailable financial marke nents will increase compet the avail. abl urces of f services t o the syste example,the required minimum paid-up capital. 18 Financial Sector Assessment: A Handbook 1 I H G F E D C B A 12 11 10 9 8 7 6 5 4 3 2 2.1.3 Competition, Concentration, and Efficiency Competition in the financial system can be defined as the extent to which financial markets are contestable and the extent to which consumers can choose a wide range of financial services from a variety of providers. Competition is often a desirable feature because it normally leads to increased institutional efficiency, lower costs for clients, and improvements in the quality and range of financial services provided. There are numerous measures of competition, including the total number of financial institutions, changes in market share, ease of entry, price of services, and so forth. In addition, the degree of diversity of the financial system could be an indicator of competition or the lack thereof because the emergence of vibrant non-bank intermediaries and capital markets often have been a source of effective competition for banking systems in many countries. All things remaining equal, an increase in the number of financial institutions or an expansion in available financial market instruments will increase competition by expanding the available sources of financial services that consumers can access. Ease of entry into the system could be judged by looking at the regulatory and policy requirements for licensing, for example, the required minimum paid-up capital. Table 2.1. Sectoral Indicators of Financial Development Sub-sector Indicator Banking • Total number of banks • Number of branches and outlets • Number of branches/thousand population • Bank deposits/GDP (%) • Bank assets/total financial assets (%) • Bank assets/GDP (%) Insurance • Number of insurance companies • Gross premiums/GDP (%) • Gross life premiums/GDP (%) • Gross non-life premiums/GDP (%) Pensions • Types of pension plans • Percentage of labor force covered by pensions • Pension fund assets/GDP (%) • Pension fund assets/total financial assets (%) Mortgage • Mortgage assets/total financial assets • Mortgage debt stock/GDP Leasing • Leased assets/total domestic investment Money markets • Types and value of money market instruments • New issues and growth in outstanding value • Number and value of daily (weekly) transactions in the instruments Foreign exchange markets • Volume and value of daily foreign exchange transactions • Adequacy of foreign exchange (reserves in months of imports, as ratio to short-term external debt or to broad money) Capital markets • Number of listed securities (bonds and equities) • Share of households, corporations, banks, and NBFIs in the holdings of securities • Number and value of new issues (bonds and equities) • Market capitalization/GDP (%) • Value traded/market capitalization (%) • Size of derivative markets Colllective investment funds • Types and number of schemes (unique and mixed funds) • Total assets and growth rates (nominal and as percentage of GDP) • Total number of investors and average balance per investor • Share of households, corporations, banks, and NBFIs, in total mutual funds assets