正在加载图片...

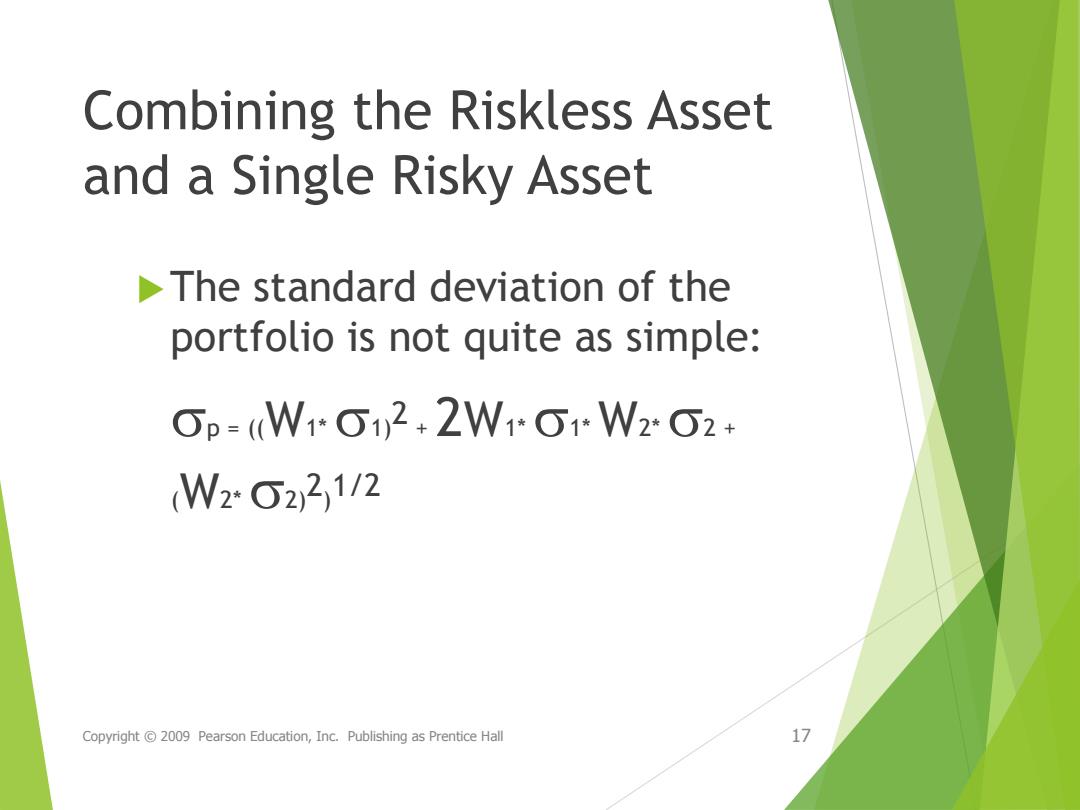

Combining the Riskless Asset and a single Risky Asset The standard deviation of the portfolio is not quite as simple: p=W1*1)2+2W1G1W2G2+ W2*G22112 Copyright 2009 Pearson Education,Inc.Publishing as Prentice Hall 17Combining the Riskless Asset and a Single Risky Asset The standard deviation of the portfolio is not quite as simple: sp = ((W1*s1)2 + 2W1*s1* W2*s2 + (W2*s2)2)1/2 Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall 17