正在加载图片...

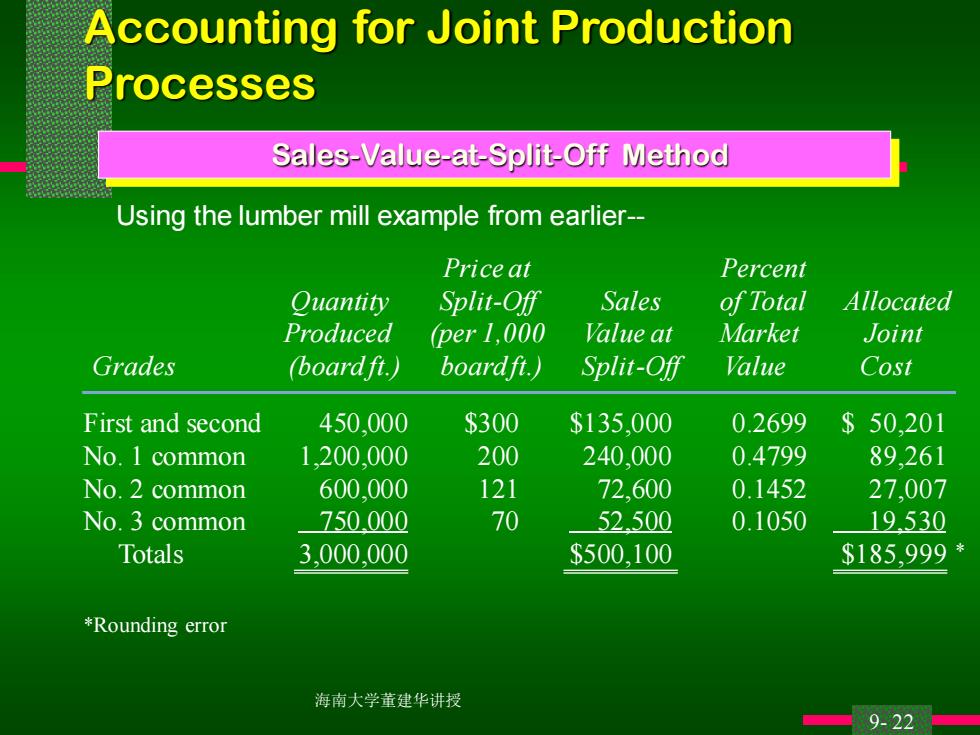

Accounting for Joint Production Processes Sales-Value-at-Split-Off Method Using the lumber mill example from earlier- Price at Percent Quantity Split-Off Sales of Total Allocated Produced (per 1,000 Value at Market Joint Grades (boardfi.) boardfi.) Split-Off Value Cost First and second 450.000 $300 $135,000 0.2699 $50,201 No.1 common 1,200,000 200 240.000 0.4799 89,261 No.2 common 600,000 121 72,600 0.1452 27,007 No.3 common 750.000 70 52.500 0.1050 19.530 Totals 3,000,000 $500,100 $185,999 *Rounding error 海南大学董建华讲授 9-22■海南大学董建华讲授 9- 22 Using the lumber mill example from earlier- Price at Percent Quantity Split-Off Sales of Total Allocated Produced (per 1,000 Value at Market Joint Grades (board ft.) board ft.) Split-Off Value Cost First and second 450,000 $300 $135,000 0.2699 $ 50,201 No. 1 common 1,200,000 200 240,000 0.4799 89,261 No. 2 common 600,000 121 72,600 0.1452 27,007 No. 3 common 750,000 70 52,500 0.1050 19,530 Totals 3,000,000 $500,100 $185,999 * *Rounding error Accounting for Joint Production Processes Sales-Value-at-Split-Off Method