正在加载图片...

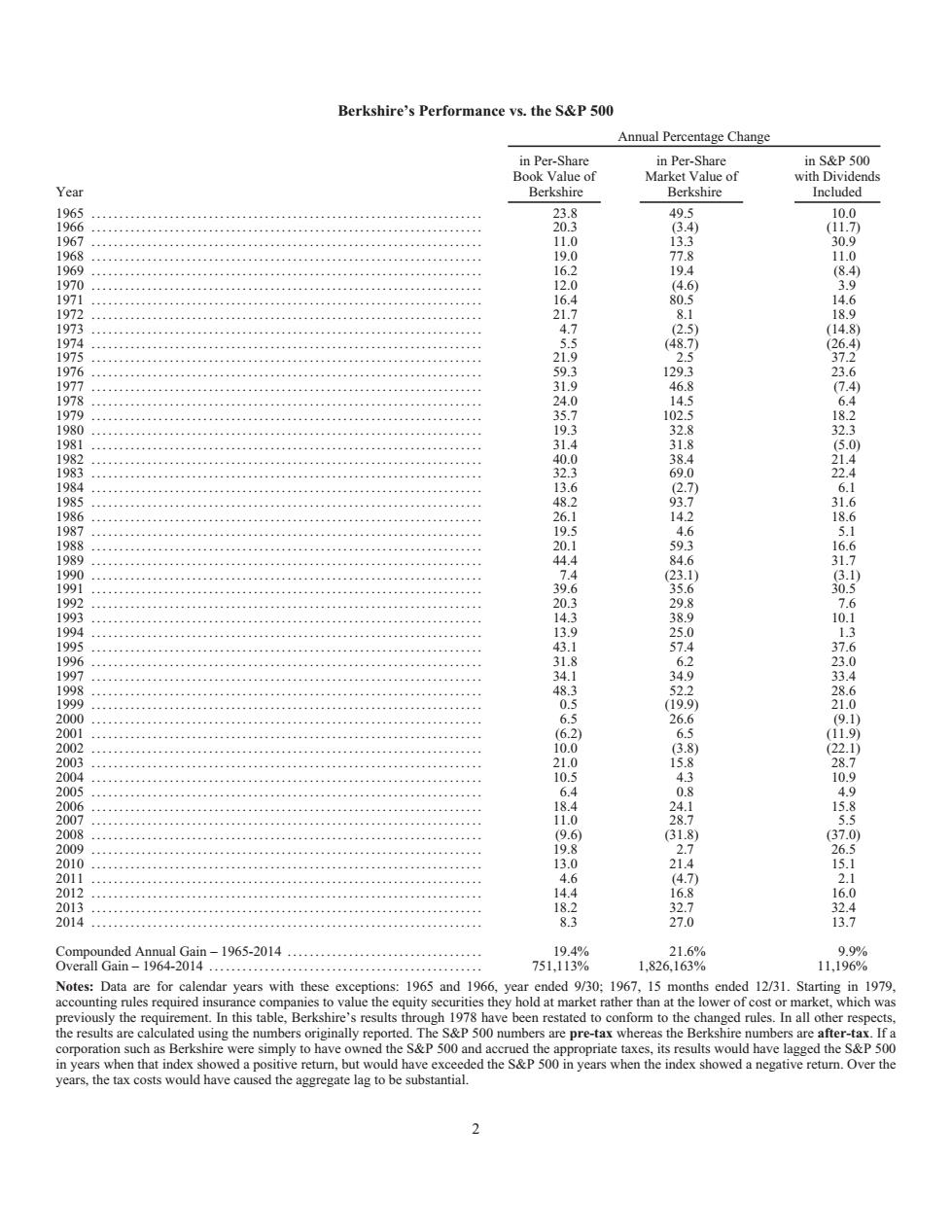

Berkshire's Performance vs.the &P500 Annual Percentage Change Bin Per-s n S&P 500 of with nd 75194 L.8266 19% Note rs with thes 1965amd196 d9/30:1967, 1ded12/31.S3 culated using the numbe e are pre-t the s are afte d ha SRBerkshire’s Performance vs. the S&P 500 Annual Percentage Change Year in Per-Share Book Value of Berkshire in Per-Share Market Value of Berkshire in S&P 500 with Dividends Included 1965 ...................................................................... 23.8 49.5 10.0 1966 ...................................................................... 20.3 (3.4) (11.7) 1967 ...................................................................... 11.0 13.3 30.9 1968 ...................................................................... 19.0 77.8 11.0 1969 ...................................................................... 16.2 19.4 (8.4) 1970 ...................................................................... 12.0 (4.6) 3.9 1971 ...................................................................... 16.4 80.5 14.6 1972 ...................................................................... 21.7 8.1 18.9 1973 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.7 (2.5) (14.8) 1974 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5.5 (48.7) (26.4) 1975 ...................................................................... 21.9 2.5 37.2 1976 ...................................................................... 59.3 129.3 23.6 1977 ...................................................................... 31.9 46.8 (7.4) 1978 ...................................................................... 24.0 14.5 6.4 1979 ...................................................................... 35.7 102.5 18.2 1980 ...................................................................... 19.3 32.8 32.3 1981 ...................................................................... 31.4 31.8 (5.0) 1982 ...................................................................... 40.0 38.4 21.4 1983 ...................................................................... 32.3 69.0 22.4 1984 ...................................................................... 13.6 (2.7) 6.1 1985 ...................................................................... 48.2 93.7 31.6 1986 ...................................................................... 26.1 14.2 18.6 1987 ...................................................................... 19.5 4.6 5.1 1988 ...................................................................... 20.1 59.3 16.6 1989 ...................................................................... 44.4 84.6 31.7 1990 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7.4 (23.1) (3.1) 1991 ...................................................................... 39.6 35.6 30.5 1992 ...................................................................... 20.3 29.8 7.6 1993 ...................................................................... 14.3 38.9 10.1 1994 ...................................................................... 13.9 25.0 1.3 1995 ...................................................................... 43.1 57.4 37.6 1996 ...................................................................... 31.8 6.2 23.0 1997 ...................................................................... 34.1 34.9 33.4 1998 ...................................................................... 48.3 52.2 28.6 1999 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.5 (19.9) 21.0 2000 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.5 26.6 (9.1) 2001 ...................................................................... (6.2) 6.5 (11.9) 2002 ...................................................................... 10.0 (3.8) (22.1) 2003 ...................................................................... 21.0 15.8 28.7 2004 ...................................................................... 10.5 4.3 10.9 2005 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6.4 0.8 4.9 2006 ...................................................................... 18.4 24.1 15.8 2007 ...................................................................... 11.0 28.7 5.5 2008 ...................................................................... (9.6) (31.8) (37.0) 2009 ...................................................................... 19.8 2.7 26.5 2010 ...................................................................... 13.0 21.4 15.1 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4.6 (4.7) 2.1 2012 ...................................................................... 14.4 16.8 16.0 2013 ...................................................................... 18.2 32.7 32.4 2014 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8.3 27.0 13.7 Compounded Annual Gain – 1965-2014 ................................... 19.4% 21.6% 9.9% Overall Gain – 1964-2014 ................................................. 751,113% 1,826,163% 11,196% Notes: Data are for calendar years with these exceptions: 1965 and 1966, year ended 9/30; 1967, 15 months ended 12/31. Starting in 1979, accounting rules required insurance companies to value the equity securities they hold at market rather than at the lower of cost or market, which was previously the requirement. In this table, Berkshire’s results through 1978 have been restated to conform to the changed rules. In all other respects, the results are calculated using the numbers originally reported. The S&P 500 numbers are pre-tax whereas the Berkshire numbers are after-tax. If a corporation such as Berkshire were simply to have owned the S&P 500 and accrued the appropriate taxes, its results would have lagged the S&P 500 in years when that index showed a positive return, but would have exceeded the S&P 500 in years when the index showed a negative return. Over the years, the tax costs would have caused the aggregate lag to be substantial. 2