正在加载图片...

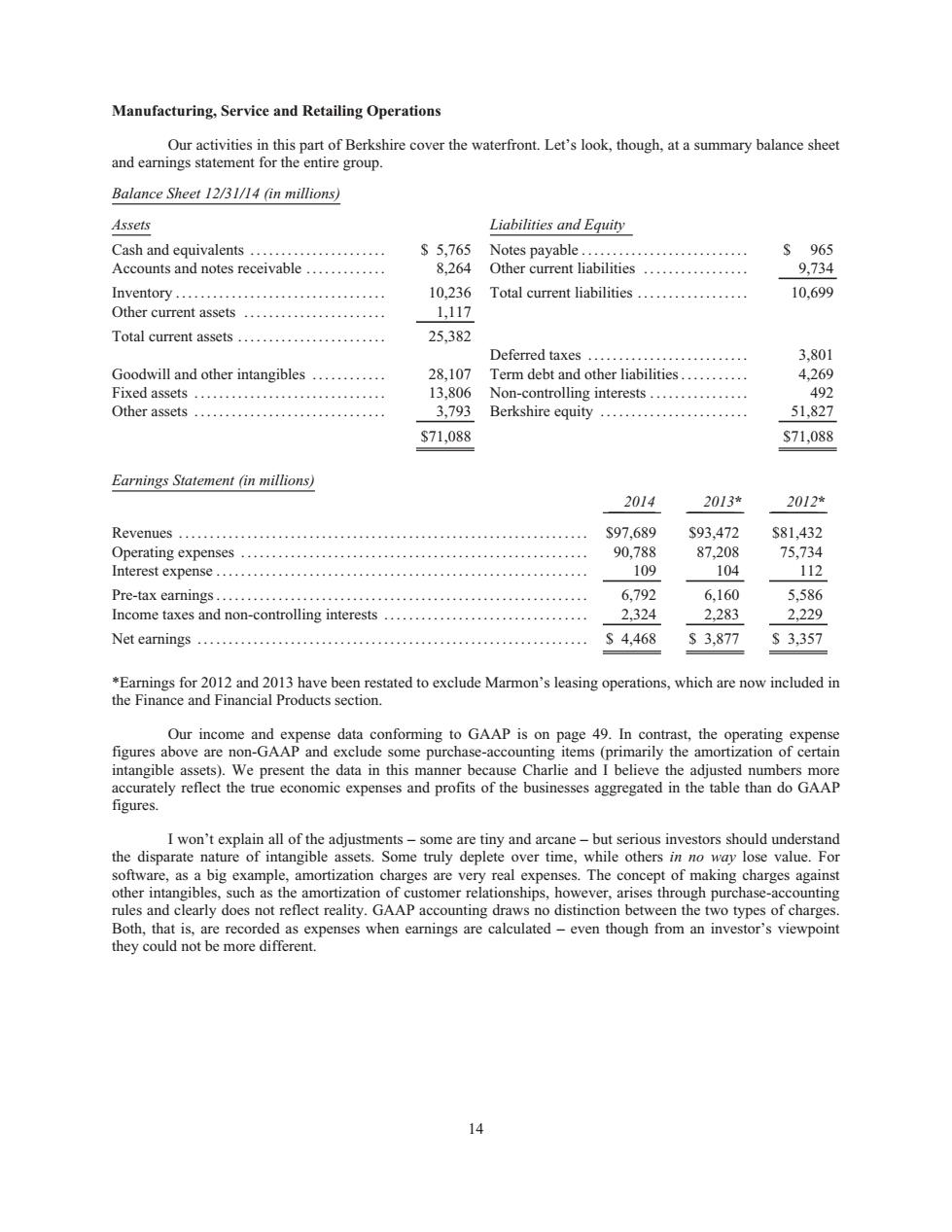

Manufacturing,Service and Retailing Operations Our activities in this part of Berkshire cover the waterfront.Let's look,though,at a summary balance sheet and eamings statement for theentire group. Balance Sheet 12/31/14 (in millions) Assets Liabilities and Equity Cash and equivalents s5,765 Notes payable S965 Accounts and notes receivable............. 8.264 Other current liabilities... 9.734 Inventory.... 10236 Total current liabilities ................. 10.699 Other current assets 1.117 Total current assets 25.382 Deferred taxes 3.801 Goodwill and other intangibles..... 28107 Term debt and other liabilities... 4,269 9 S71,088 S71,088 Earnings Statement (in millions) 2014 2013 2012* Revenues $97.689 S93.472 S81,432 Operating expenses....... 90,788 87.208 75,734 Interest expense.......................................................... 104 112 Pre-tax earnings. 6.79 6,160 5,586 Income taxes and non-controlling interests ............................... 2.324 2.283 2,229 Net earnings. s4.468 S3.877 S3,357 Our inc and data onforming to gaap is on 49.n data in this manner r bec I won't evnlain all ofthe adi the disparate nature of intangible as oftware,as a big example,amortizatior arges are very real The of making charges agains rules and learly does not reflect reality.GAAP accounting draws no distinction between the two types of chargeManufacturing, Service and Retailing Operations Our activities in this part of Berkshire cover the waterfront. Let’s look, though, at a summary balance sheet and earnings statement for the entire group. Balance Sheet 12/31/14 (in millions) Assets Liabilities and Equity Cash and equivalents ...................... $ 5,765 Notes payable . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 965 Accounts and notes receivable ............. 8,264 Other current liabilities ................. 9,734 Inventory .................................. 10,236 Total current liabilities .................. 10,699 Other current assets ....................... 1,117 Total current assets ........................ 25,382 Deferred taxes .......................... 3,801 Goodwill and other intangibles ............ 28,107 Term debt and other liabilities........... 4,269 Fixed assets ............................... 13,806 Non-controlling interests . . . . . . . . . . . . . . . . 492 Other assets ............................... 3,793 Berkshire equity ........................ 51,827 $71,088 $71,088 Earnings Statement (in millions) 2014 2013* 2012* Revenues .................................................................. $97,689 $93,472 $81,432 Operating expenses ........................................................ 90,788 87,208 75,734 Interest expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 109 104 112 Pre-tax earnings............................................................ 6,792 6,160 5,586 Income taxes and non-controlling interests ................................. 2,324 2,283 2,229 Net earnings ............................................................... $ 4,468 $ 3,877 $ 3,357 *Earnings for 2012 and 2013 have been restated to exclude Marmon’s leasing operations, which are now included in the Finance and Financial Products section. Our income and expense data conforming to GAAP is on page 49. In contrast, the operating expense figures above are non-GAAP and exclude some purchase-accounting items (primarily the amortization of certain intangible assets). We present the data in this manner because Charlie and I believe the adjusted numbers more accurately reflect the true economic expenses and profits of the businesses aggregated in the table than do GAAP figures. I won’t explain all of the adjustments – some are tiny and arcane – but serious investors should understand the disparate nature of intangible assets. Some truly deplete over time, while others in no way lose value. For software, as a big example, amortization charges are very real expenses. The concept of making charges against other intangibles, such as the amortization of customer relationships, however, arises through purchase-accounting rules and clearly does not reflect reality. GAAP accounting draws no distinction between the two types of charges. Both, that is, are recorded as expenses when earnings are calculated – even though from an investor’s viewpoint they could not be more different. 14